This article has been written by Jack Warchalowski, a world-leading expert in Demand Driven Replenishment (DDR) and the application of the Theory of Constraints (TOC) to the supply chain and manufacturing operations. Jack has prepared a DDR Data Feed Download that includes Results and an Implementation Snapshot of the practical application of DDR in action.

This article has been written by Jack Warchalowski, a world-leading expert in Demand Driven Replenishment (DDR) and the application of the Theory of Constraints (TOC) to the supply chain and manufacturing operations. Jack has prepared a DDR Data Feed Download that includes Results and an Implementation Snapshot of the practical application of DDR in action.

Free download.

Why traditional cost-per-unit analysis is actively undermining your business success!

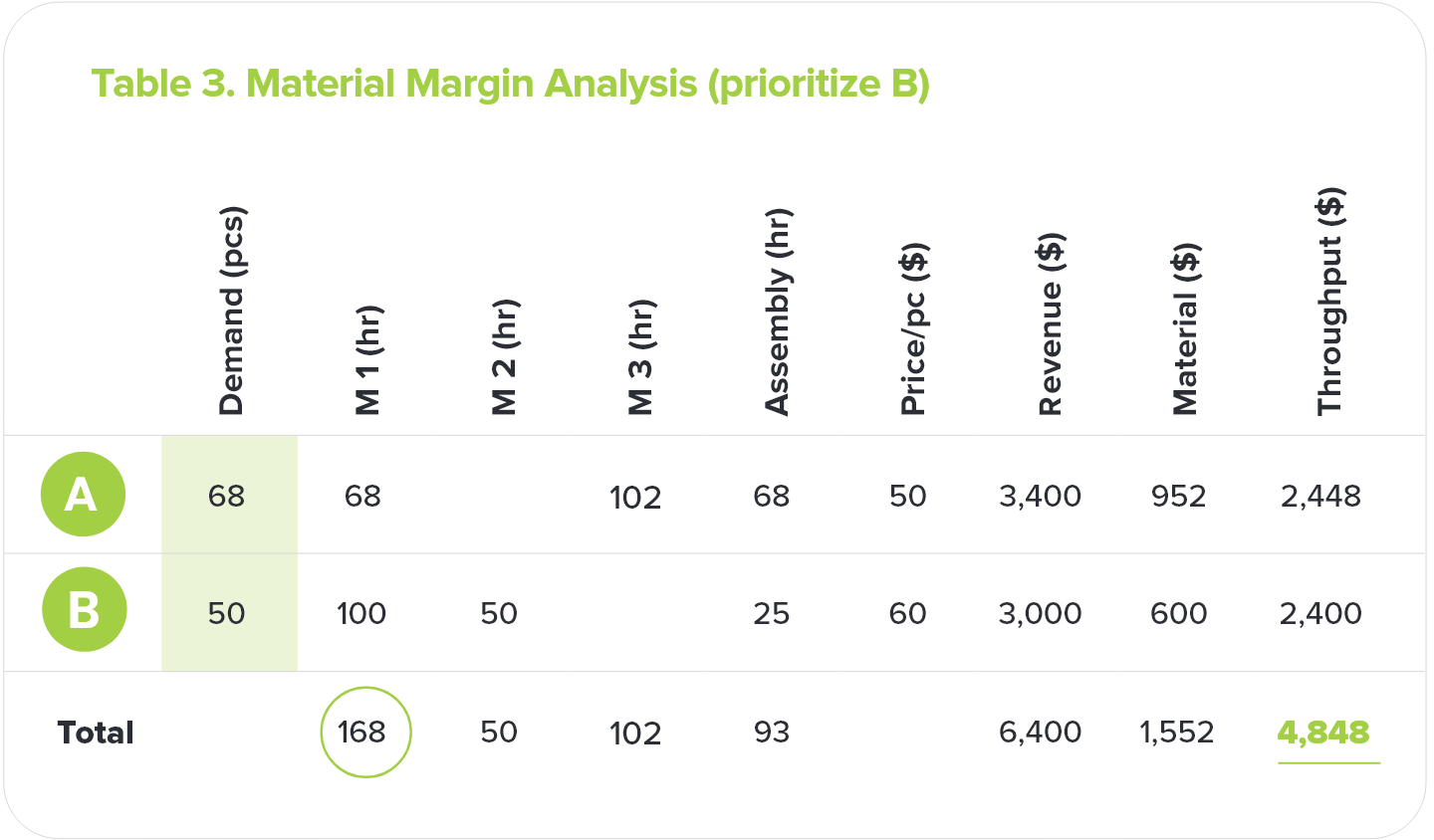

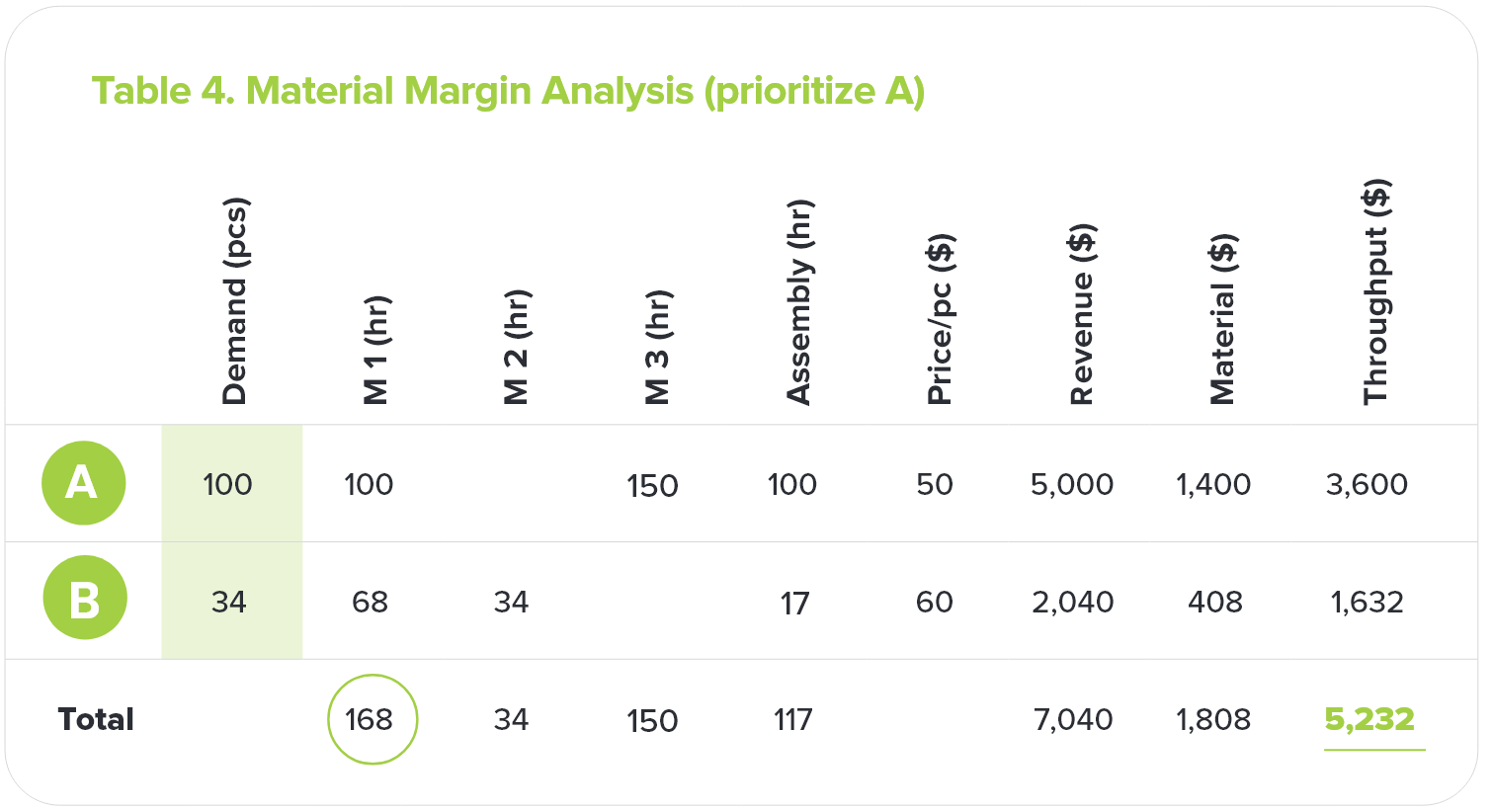

Cost-per-unit, the world’s most popular analysis process, is a devastating and flawed paradigm of traditional business decision making.

Cost-per-unit allows managers to use the concept of gross margin or contribution margin to evaluate business opportunities. It enables a simple process for decision-making. That’s why it’s very popular.

An illustration of the gross margin fallacy

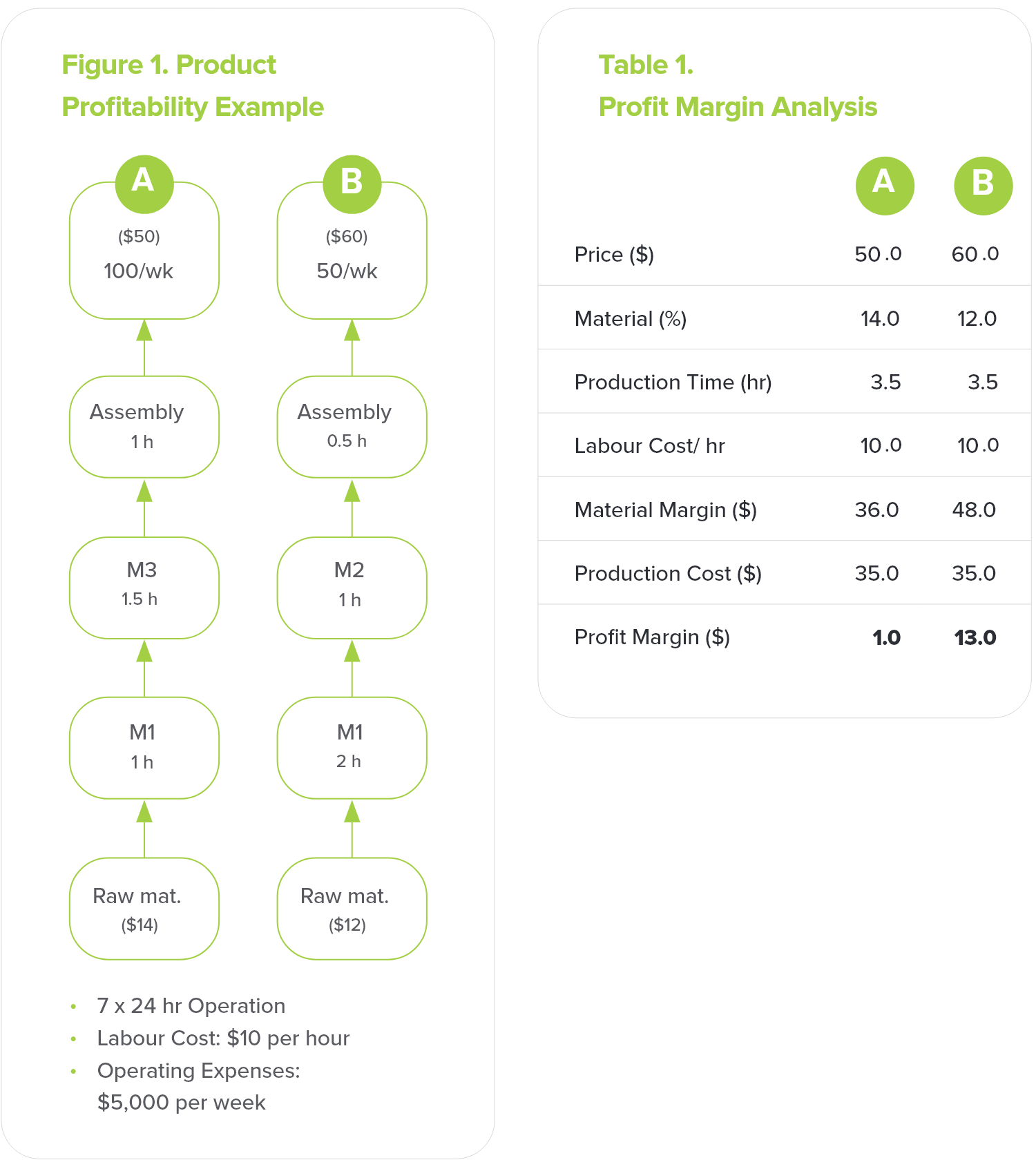

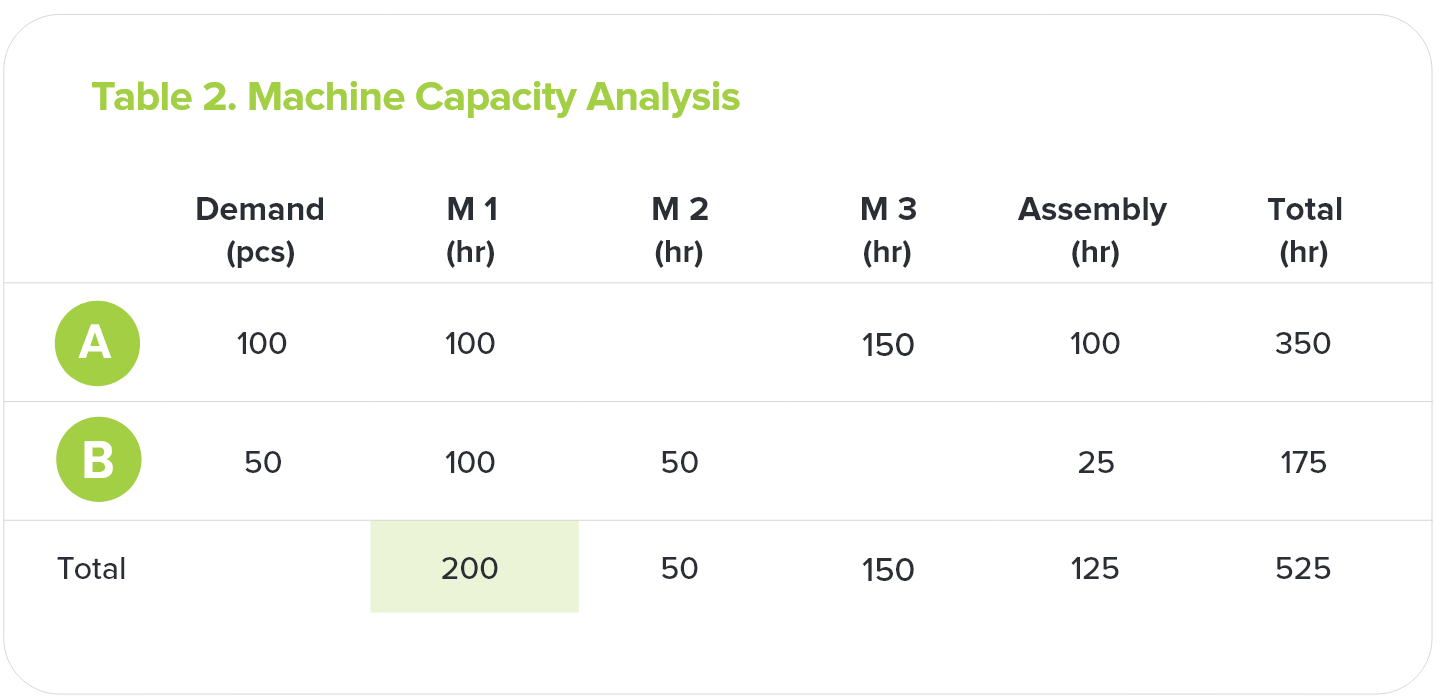

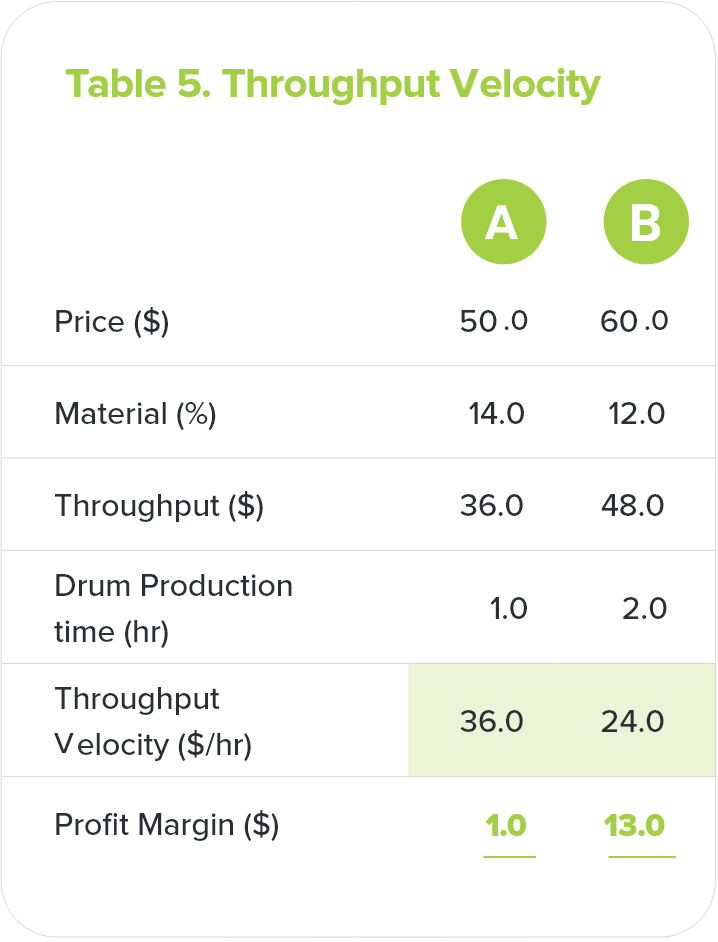

Consider a company that produces only 2 products: A and B (shown below in Figure 1). This company runs a 7 x 24hr operation, with a labour cost of $10 per hr and Operating Expenses of $5,000 per week.

Product A is produced from Raw Materials costing $14 per unit. Product A is processed on Machine 1, Machine 3 and a Final Assembly operation at the rates specified below. It is sold for $50 each and its demand is 100 per week.

Product A is produced from Raw Materials costing $14 per unit. Product A is processed on Machine 1, Machine 3 and a Final Assembly operation at the rates specified below. It is sold for $50 each and its demand is 100 per week.

Product B is produced from Raw Materials costing $12 per unit. Product B requires Machine 1, Machine 2 and the Final Assembly at the rates also specified below. It is sold for $60 each and its demand is 50 per week.

Product B is produced from Raw Materials costing $12 per unit. Product B requires Machine 1, Machine 2 and the Final Assembly at the rates also specified below. It is sold for $60 each and its demand is 50 per week.

This article has been written by Jack Warchalowski, a world-leading expert in Demand Driven Replenishment (DDR) and the application of the Theory of Constraints (TOC) to the supply chain and manufacturing operations. Jack has prepared a DDR Data Feed Download that includes Results and an Implementation Snapshot of the practical application of DDR in action.

Free download.